Where are we up to now?

For those firms who have already been through this year’s renewal process, most of you will have been pleased to see the effects of the changing market cycle on your insurance premiums. All other things remaining equal, you will likely be paying no more than last year and, in many cases, you will be paying less. The rating ‘plateau’ we saw last year has now definitely changed into a downhill trend of reductions.

Given the increases in cost that we’ve all faced since 2018 – and we include ourselves in this category as buyers of our own PI insurance – the promise of the PI market coming off the boil and the market cycle moving on to its next phase is very welcome.

Although individual renewals will, as ever, turn on factors specific to your business, such as: claims performance, fee revenue changes, or changes in the composition of your income, we’re very sure that unlike previous years, most will be receiving some good news which will help amongst other things with the recent changes to NI.

Why?

We would love to say that the huge amount of work our teams have done, particularly over the last five years, in trying to change the risk environment for engineers, architects and all those engaged in the design of the built environment have borne fruit . Those in the sector who have followed our work will have heard of our recent Constructing Change initiative, where we set out the problems facing our clients and our proposed solutions to those problems. That work continues and we are pleased to see industry bodies begin to grapple with how to take some of these ideas forward, with our continued support.

The reality is, however, that whilst we are rightly proud of our efforts to make the world in which you work a better, safer and less risky place, that is not the catalyst for the changes we are currently seeing in the market. At least not today.

The reality is far more prosaic: the PI market cycle.

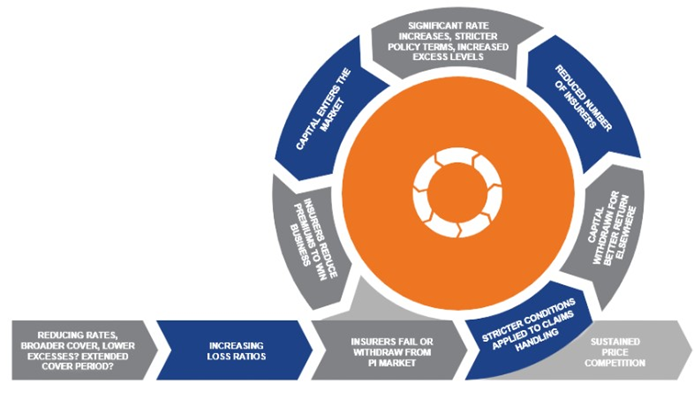

Anyone who has been in the business of buying PI insurance for any length of time will have come across this phenomenon of the Construction PI market and we reproduce a much used graphic to illustrate the key features:

Back in 2018/19 we began the ‘hard market’ years of insurers walking away from PI insurance because of a lack of profitability and a real fear of the claims potential associated with latent fire safety issues and worries about the insurability of UK construction PLC, highlighted in particularly difficult and distressing evidence given to the Grenfell Inquiry. We are all familiar with the rate increases and policy wording changes that followed and we don’t propose to dwell on those here.

History tells us what follows any sustained period where insurers crash out of the market, brokers struggle to find safe harbour, policy cover is withdrawn, and rates increase beyond affordability. What follows is a period where those insurers who couldn’t support their clients during the difficult times start to come back into the market, to capitalise on the relatively high rates being charged.

New entrants, too, see opportunities to make money in a world where they have limited or no exposure to the long-tail liabilities of incumbent insurers and see their chance to make quick profits over a short period of time.

Brokers who left firms with the existential threat of not being able to source any PI cover also return to the market, with new promises of fresh (or returning) capital, cheap rates and broader cover. The last point is always worth considering in the context of the ‘claims made’ nature of PI. If today’s ‘broader cover’ can’t be sustained throughout the market cycle – as we have seen most recently with fire safety cover – then its value is questionable, at best.

These are all very well–worn themes and, as we have said previously, there is nothing new under the sun.

Whilst the increase in capacity is positive news, not all options will prove to be good choices and unfortunately history has a habit of repeating itself as our graphic and our collective experiences show.

What next?

As insurance practitioners at the coal face of construction disputes for decades, we are often presented with more opportunities than most to view the glass as being half empty. Our job is really not to see the glass at all, but to try and see the issues which are competing to fill or empty it and advise on the best course of action accordingly. This is a particular danger where perhaps more so than at any other time, thinking about what’s just over the horizon requires more crystal ball gazing than simply looking at our PI cycle graphic, or looking at hard data and claims trends.

The reason in a word is: uncertainty.

This is a feeling we have all lived with much more than we would have liked and for what now seems like a very long time. The uncertainty following the UK’s withdrawal from the European Union back in 2016. The uncertainty following the disaster at Grenfell Tower and the potential broader impact of the subsequently identified failings in the construction sector. The uncertainty following the Covid-19 pandemic and the once in a generation impact on every aspect of our lives. The uncertainty in the geopolitical environment and the impact on global supply chains.

These past uncertainties stress tested our model and our philosophy in ways no one could have anticipated. The reality is, however, that the core principles of our business allowed us, our clients, our insurance partners and our colleagues in the industry to work together to not only weather these issues, but to make something better from them. Collectively, how did we do that?

We worked:

- closely with our clients to present their risk properly and effectively to ensure their insurance protections were technically effective, globally compliant and represented value for money.

- to ensure that our clients received the best risk management advice that we could offer.

- to ensure that if our clients had claims, they were dealt with fairly.

- to advocate on our clients’ behalf at institutional and Government level to try and make their business environments fairer, safer and less volatile.

- to ensure our clients were supported by teams of specialist brokers who were connected, engaged in and deeply knowledgeable about their businesses and the world in which they work.

Which is exactly what we need to do today. Through the application of these principles, we are really dealing with the business of enabling our clients to make better decisions to support them over the long-term. If we didn’t work tirelessly to do that, we would simply have ended this market update at the part where we said you’ll very likely be paying less for your PI this year!

Today, we need to think about preparing for what might happen beyond this upcoming period of what is likely to be calmer waters. To think about, prepare for and attempt to manage beyond the coming phase of the cycle and consider what tomorrow’s uncertainties will be.

The key areas to consider include:

- the fundamental changes brought about by the building safety legislation in England and Wales. The problems around just what firms must do in order to discharge their new statutory responsibilities have been the subject of more questions to us than any other issue. That specific uncertainty is likely to only grow as the Government responds to the Grenfell Tower Inquiry’s report with more change on the way.

- the true extent of the PI insurance industry’s exposure to fire safety matters is – still – largely unknown. As the litigation now starts to begin following the conclusion of the Grenfell Inquiry’s report, we will begin to understand in the coming years whether the market has reserved sufficiently to pay the expected volume of claims and, if it hasn’t, what the market might do about it. Although it is a matter for individual consideration, the increasing availability of extended period policies needs to be carefully considered.

- the emerging risks around technology which, for years, focused on the use of Building Information Modelling are taking new dimensions in the use of artificial intelligence. As we wrote some while ago now these risks could cause upheaval in the market for lots of reasons.

- the changing macro-economic cycle and geopolitical strife which could negatively impact investment returns. Whilst investment returns in recent years have been exceedingly good for anyone investing in the global markets – including insurers – those returns are likely to be far more volatile (and possibly more negative) in the coming years. This could put greater pressure on the need for insurers to make money on a simple underwriting basis and cause fringe players to be flightier than they would otherwise be at this point of the PI cycle.

And then there are the perennial issues; consultants and architects being asked to do more for less, with continual pressure to take on greater exposure through onerous contracts and increased PI insurance requirements.

How can we prepare to meet those uncertainties?

Today, we need to ensure that you benefit from the less challenging market conditions. This means looking to derive the maximum sustainable benefit for you on cost and cover.

Tomorrow, as today, we need to continue to prioritise and to help you:

- achieve the right balance between the cost, cover and security to deliver long-term value.

- to understand your exposures and help you make informed decisions about the risks you’re taking on.

- push back when the risk v. reward balance isn’t right.

- to make better decisions about whose hands you place your insurance arrangements in, along with your trust and livelihoods

Whatever the future holds, we need only look back at the more extreme difficulties that many firms encountered in recent years to illustrate the severe consequences of blindly following the PI market cycle with little or no thought to the longer-term. Many clients who have returned to us in recent years have had firsthand experience of the problems of being promised one thing and being given another. The role of a PI broker is to apply knowledge and understanding, to help you navigate through the market and to recognise that the decisions we make today will have implications that extend well into the future.

At a time of significant uncertainty, our clients can rest assured that we will continue to be guided by a very simple philosophy and one that has served them well at all points in the market cycle – we do what is in our clients’ best interests.

If you are a client of ours and would like to hear more, then do please get in touch with your usual G&A contact. For those of you who would like to experience the Griffiths & Armour difference, do please get in touch with us and we will be very happy to assist further.

Griffiths & Armour, Authorised and regulated by the Financial Conduct Authority in the United Kingdom. Head Office: 12 Princes Parade Princes Dock Liverpool L3 1BG

Partners: Griffiths & Armour Ltd Aon UK Ltd

VAT No. 480840148 An Aon company

Some links on this website may redirect you to third party sites, Griffiths & Armour is not responsible for this content.

FP.GA.2025.1.CC

Whilst care has been taken in the production of this article and the information contained within it has been obtained from sources that Griffiths & Armour, an Aon company believes to be reliable, Griffiths & Armour, an Aon company does not warrant, represent or guarantee the accuracy, adequacy, completeness or fitness for any purpose of the article or any part of it and can accept no liability for any loss incurred in any way whatsoever by any person who may rely on it. In any case any recipient shall be entirely responsible for the use to which it puts this article.This article has been compiled using information available to us up to 2 October 2025